|

The Celestial Wheel

An In-depth Forecast

February 1, 2010

|

Bankers -- Economic Terrorists

Bubble, Burst & Then Reform

Societal development is comprised of sequential trends, unveiled first as a sketch, and later filling in the detail -- like an artist creates a landscaping painting.

This investigative process for the new millennium began in earnest when G.W. Bush was inexplicably reelected. The December 4, 2004, The United States Through Its Planetary Cycles, Part I and Part II. unveiled a three- step process in the late nineteenth century. The First Gilded Age was followed by economic debacle which resulted in popular protests instigating reform -- the First Progressive Age. These trends are revealed the planetary cycles of the Moon and Mars. The very same sequence of planetary cycles and trends began repeating in December 1998.

This ten year Moon cycle heralded the Second Gilded Age. G.W. was reelected because he fit the part. Mars' seven year cycle began in 2008, signaling the Millennium Contraction, which has begun stimulating popular protests to bring the Second Progressive Age. The December 1, 2007 Through The Second Gilded Age offers a clear exposition of this process.

This sequence was most recently expanded upon in the January 4, 2010 In-depth Forecast, Goodbye 2009 & Into 2010, which stated,

| ...the First Progressive Age grew out of the excesses of the First Gilded Age in the 1880s, which then culminated in the Financial Panic of 1893 -- a ruinous four year depression.... The big question is whether the Second Progressive Age begins soon enough, and with enough potency to resolve Millennium Contraction problems before 2013, when the dollar will otherwise collapse under government debt. The stimulus for this must come from the grass roots, as really all major social and political movements have -- through popular protests. |

In the nineteenth century's First Gilded Age, excess and risky lending by banks for housing and railroads led to the Financial Panic of 1893. From this, the sight of the vacant Victorian (haunted) house entered the American mindset. The twenty-first century's Millennium Contraction's housing bubble and auto industry collapse parallels amazingly.

Bankers -- Economic Terrorists

As in the nineteenth century, the bankers are economic terrorists. They hold our money deposited in trust with them, and they gamble it away to our loss. Banking is a unique industry. It promises a safe place to place our money and then lends it out to businesses and individuals to enable economic development. Unlike other industries, which are supported by limited financial interests, banks are financed by everyone. When they lose, the entire population suffers.

Some have pointed the finger at others -- borrowers, mortgage brokers, government regulators and public mortgage holders like Fannie Mae, greedy developers, ineffective auto industry management, too-powerful labor unions... But, the bottom line is that all the gluttonous activities that brought the Gilded Ages were bankers-enabled. Their greedy irresponsible lending was the source of the excess and the consequently ruinous economic bubble.

It's like Mom put a big bowl of candy (the family savings) on the table, and the children (borrowers) grabbed it all. The savings were lost, and the children had stomach aches. They then get their stomachs pumped in the emergency room.

As described above, popular protests from the grass roots are essential to the process of reversing this tide of greed and economic unfairness that is ruining the economy. As banks are the economic terrorists, they must be the primary target of popular protests.

There are hundreds, if not thousands, of news reports about the excesses of the financial sector, but this one really reveals the essence of the economic terrorists, U.S. financial companies paid $145 billion in 2009. That's an 18% increase from 2008, during the worst economic year since the Great Depression. The amount is obscene and is a slap in the face to every American. And if these facts aren't enough to boil the blood, the $145 billion amounts to $483 per person.

This is like a bank armored truck pulled up to your house requiring you for $483 for each resident.

Read Paul Volcker's How to Reform Our Financial System. Volcker is a past chairman of the S.E.C. and current chairman of the administration's Economic Recovery Advisory Board. After a year of listening to the bankers, President Obama is finally paying attention to Volcker's wise counsel. He's really saying the same things as this Celestial Wheel, but is more polite.

Unabated Banker Greed

The bankers weren't finished with bleeding us after the Millennium Contraction began really tightening the screws in late 2008. Suffering losses themselves from non-performing mortgages and fancy gambling investments they created like credit default swaps, the banks began gouging credit card holders with increased fees, penalties and interest rates -- even as consumers were also under duress in these areas as Millennium Contraction hit. The Celestial Wheel, having seen this comings as well, cautioned in the October 8, 2007 Commentary,

| As the banks continue to experience dropping profits, their Enron-greedy executives will look to bank credit card divisions to replace real estate mortgage losses. Part of their strategy relates to consumers resorting to credit cards because home equity loans are no longer available. That is, the banks know very well consumers are relying upon plastic more than ever, which means consumers are very obedient in making credit card payments and won't challenge fees -- for fear of losing this last source of borrowing. So, the banks will be very aggressive: hiking fees, adding new fees, raising interest rates and fraudulent schemes -- like holding your payment check until after the payment due date and having payments due on a holiday. Watch your credit card statements carefully, preferably on-line, to catch any of these increases and protest any unfair charges. The reality is, the banks need you to have credit cards just as much as you need them to survive cash shortfalls. |

Bankers Mining Our Deposits

There was a final gold vein another for these economic terrorist to mine -- overdraft protection. This is the most egregious of all, for these are not loans for which consumers must pay -- but our own dollars deposited in trust with the banks that they then hit with fees, which can only be termed abusive.

Well, from the greedy bankers' view, this was the last source of wealth to steal. By making overdraft protection automatic, and encouraging the use of debit cards, checking account holders frequently went into the red. This unleashed a flood overdraft fees, $38 billion annually, $110 per person in America. There's great irony here, for the term overdraft protection actually results in overdraft theft.

However, in response to consumer protests, the government is closing that gold vein. On November 12, the Federal Reserve announces final rules that prohibit financial institutions from charging consumers fees for paying overdrafts on automated teller machine (ATM) and one-time debit card transactions, unless a consumer consents, or opts in, to the overdraft service for those types of transactions.

The banks are naturally worried about these upcoming rules stopping them from raiding this cookie jar and began pro-acting, although as explained below, this is just a ruse. Tired of $30 overdraft fees? Just say ‘no thanks’! explains,

| Starting Oct. 19, Bank of America customers could begin opting out of automatic overdraft services and the bank will only charge for such services if the account dips below -$10. BofA will also cap the number of transactions that can occur after an account dips below zero in June. At the beginning of next year, Chase said it would stop an industry-standard practice of processing each day’s transactions from highest to lowest — and therefore incurring more overage charges should the balance drop below zero. |

See, Chase and Bank of America Revise Fee Policies for specifics.

The January 20, 2010, Haiti -- A Metaphor & More, included sections on money, including, Floating Your Debit Card Charges. It explains how to use the Visa/Mastercard system to avoid overdraft fees ...if your checking account is getting low, you can float a debit card charge for two business days, to reduce the risk of a $35 overdraft fee. Remember that "signature debit" sends the charge through the credit card payment system (Visa or Mastercard) before it is submitted to your bank to charge your checking account. This takes two days. This author knows the method works because he has frequently used the signature debit float to avoid overdraft fees and checks his on-line statement each morning.

Well, dealing with economic terrorists banks really is like fighting other terrorists -- a chess game of moves and countermoves. Even as some banks are already back-peddling on their most egregious policies before the government forces them to, at least one has already figured out how to mine this gold vein from a new angle! (And here's another, which the State of N.Y. caught, Citigroup in settlement on checking account fees.) They do this by first processing all charges and then later processing credits -- falsely forcing account balances below zero to enable charging the overdraft fee. That's the ruse.

Note the difference:

...industry-standard practice of processing each day’s transactions from highest to lowest — and therefore incurring more overage charges should the balance drop below zero.

...first processing charges and then later processing credits -- falsely forcing account balances

below zero to enable charging the overdraft fee.

The next section documents how National Bank Of Arizona changed to that fraudulent bookkeeping policy to generate ore overdraft fees, -- just a few days after The Celestial Wheel made the suggestion how do dodge those fees!

While The Celestial Wheel has protested for years by revealing these malfeasances, its time to actively protest on this web site. The below case fully documents the theft -- and there's no milder word to describe it.

The Celestial Wheel Protests

Although the Celestial Wheel has correctly predicted this three-step trend from bubble to bust to reform, and has correctly identified the banks as economic terrorists, the author has not yet used this alternative media platform to protest against the banks. Now is the time to move from explaining to complaining, from describing to protesting.

Banks close their daily books at 3 PM, the traditional time for their offices lock the door. Charges and credits come in during the day and keep arriving electronically. They process all of these during the night to arrive at day-ending account balances the next morning before they re-open at 9 AM. Charges that come in after-hours include automatic withdrawals, checks that clear and signature debit. After-hours credits include automatic deposits (pay checks....), ATM deposits and retail merchants credit/debit card payments. (Note; this is exactly how hotels work. You check-in with a payment, incur restaurant and other charges. The night audit posts these and your room charge to arrive at a balance the next morning.)

As explained above, banks' standard practice has been to post all charges from highest to lowest to force checking accounts into the red. Credits would be posted chronologically -- as they came in. The new practice is to post all charges first to force even more negative balances -- and then post credits. The former method generated $38 billion in overdraft fees last year. The new method promises to criminally extract much more.

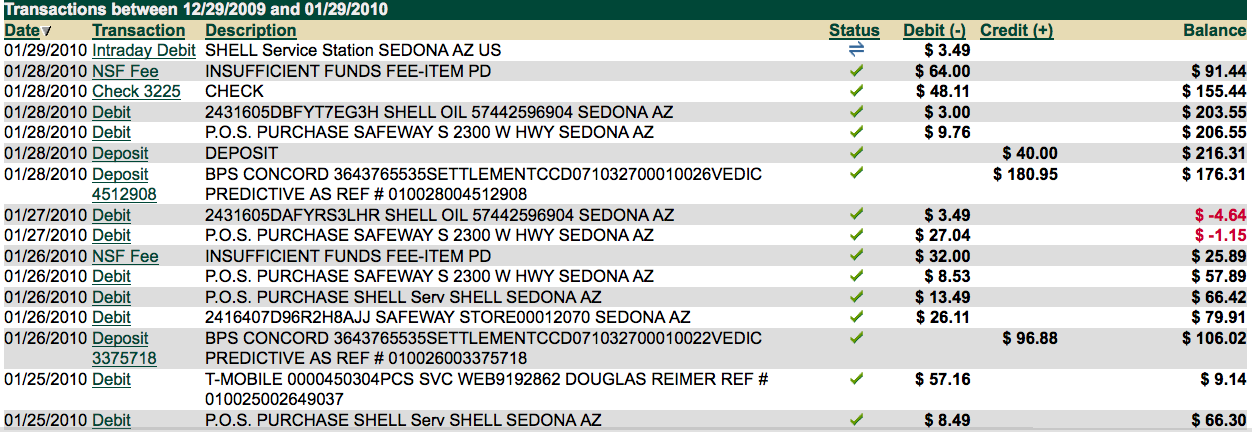

The below on-line statement from National Bank of Arizona shows the this new ruse in action:

1. 1/25 Beginning balance $66.42. T-Mobile automatic withdrawal $57.16. Final balance $9.14

2. 1/26 Beginning balance $9.14. BPS retail merchant credit $96.88. Safeway signature debit from 1/24 $26.11. Shell debit $13.49. Safeway deibt $8.53. Balance $57.89. Then, comes a $32 insufficient funds charge. Final balance $25.89.

3. 1/27 Beginning balance $25.89. Safeway debit $27.04 at 5:15 PM. ATM cash deposit $40 at 5:34 PM (Would have been sooner but there were no envelopes at the ATM machine. Also, ATM deposits are required to give immediate credit up to $100, which was not done.) Shell signature debit 1/25 $3.49. Interim balance $1.15 Final balance $4.64. ATM cash deposit was not credited until the following day. Correct balance was $35.36

4. 1/28. ATM cash deposit, BPS retail merchant credit, a check cleared, a shell debit and two insufficient funds fees from the previous day of $64.